In the previous blog posts, we took a brief look at how you can buy the perfect car insurance policy at a lower price.

We opened our magical box of secrets and revealed some amazing tricks that can help you buy a car insurance policy at a comparatively lower price.

Can you tell us what else did we learn?

Car Insurance Coverage!

That’s what you are forgetting.

And if you are thinking about buying a car, the first thing you should do right now is to educate yourself with everything there is about the “Car Insurance” concept.

If you don’t, you’ll not know which policy is the perfect one for you. Plus, you won’t even be able to decide which coverages you need

What’s required?

What’s optional?

You might get seriously confused, and we don’t want that to happen.

If you ask us whether it’s indispensable to know about all of this stuff, then let me tell you this.

If you want to save some bucks, you should educate yourself with it right now.

If you don’t know what’s required and what’s optional, you’ll pretty much buy all of it.

And it means that you are merely wasting your money.

And if you understand the coverages that fit your lifestyle, nothing can stop you from saving some few bucks.

And that’s what we will cover in this article.

Without wasting any further time, let’s just get started right away!

Car Insurance Coverage Types

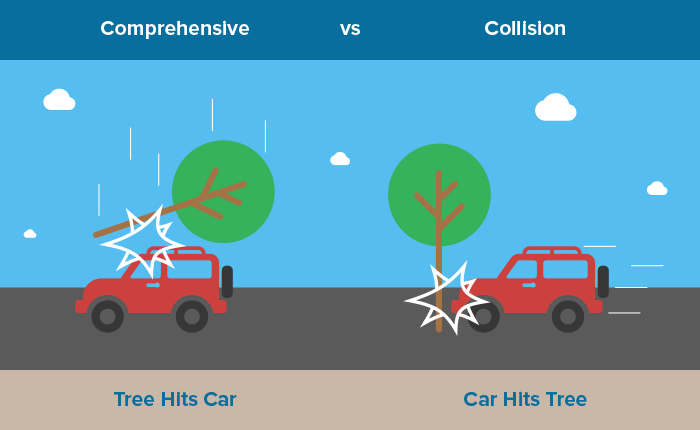

Comprehensive Coverage

Don’t get confused right here!

Judging by its name, don’t assume that this coverage will cover everything there is.

You might think that it covers everything literally and later learn that you were wrong.

When it comes to car insurance, it’s a different case.

Let’s learn what comprehensive coverage is.

With the help of comprehensive coverage, you will be able to claim for damages that take place due to something other than an accident with another vehicle.

Let’s just suppose that a tree fell on your car.

And your car is now pretty much damaged. Maybe, it’s crushed.

And that’s where comprehensive coverage comes to rescue.

Animals! Natural Calamities! Theft! Riots! Vandalism!

These are some of the cases in which you can load up the “Comprehensive Coverage” bullet in your gun.

Comprehensive coverage won’t pay for your medical bills or damage to another person’s vehicle.

If you run your car into a building or any object, then you won’t be able to load up the comprehensive coverage.

Whether to buy it or not depends on how old your car is.

If you think that your car is pretty old and has a short lifeline, then you should avoid buying this coverage.

In case you recently bought a brand-new car, nothing should stop you from including it in your car insurance policy.

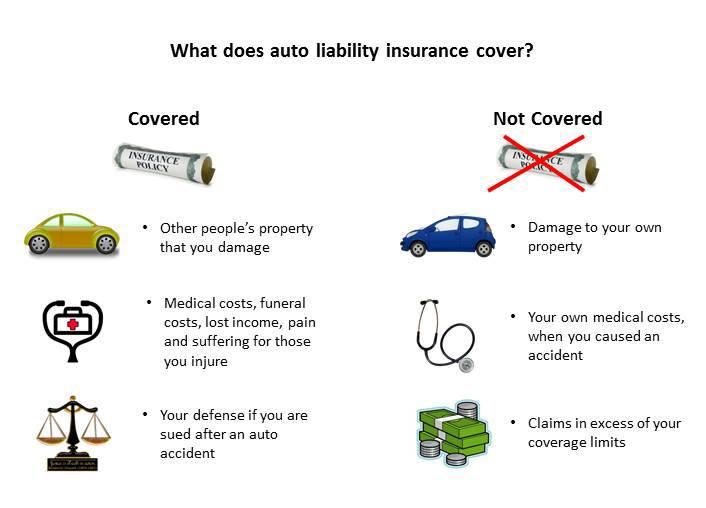

Liability

Let’s just assume that you are involved in a car accident.

The chances are that the fault is yours.

In such a scenario, you’ll be liable for all the damages.

And nothing would make you happier than the words, “It’s all covered” in such a case.

What liability insurance will do for you is that it will cover the other person’s medical expenses and the auto repairs cost.

We often refer it to as “Minimum coverage.”

And there’s just more to it.

Let’s just dig in a little deep and explore more there is about liability.

There are a total of two kinds of liability coverage:

- Property Damage Liability Insurance

- Bodily Injury Liability Insurance

You need to buy them both.

Let’s have a little sneak-peek at each of the types.

Property Damage Liability Insurance

It covers repairs to things like dented doors and folded fenders.

Bodily Injury Liability Insurance

It covers repairs of the people. It will include the costs of physical therapy or doctor’s visits.

NOTE: Liability insurance just covers the other people’s medical and repair expenses who are involved in the accident.

Don’t mistake it for yours.

And this is the coverage that you should include in your insurance policy.

Collision Coverage

And this is the coverage that comes in when comprehensive one leaves off.

Confused, right?

That’s what we are here to explain.

Let’s just assume that you hit another object, such as another car or a light post with your vehicle.

You’d have to pay for the damages, right?

And that’s where collision coverage comes to the rescue.

Hitting an animal or a hail!

That’s not covered in the collision coverage.

And it’s a policy that covers you and not your car.

The same case is applicable when you drive your friend’s car as well.

Any car you drive, and if you hit an object or another vehicle, your expenses will be secured.

It even covers the damages to the rental car.

However, that’s applicable in some countries only.

Rollover damages as well as repairs from a hit-and-run accident.

That’s covered as well.

If you are involved in an accident that isn’t entirely covered by liability insurance, you can always bring in collision coverage.

It won’t cover the expenses for the other car or pay other people’s medical bills involved in the accident similar to liability insurance.

And if you are a new driver who doesn’t have a lot of control, you should include this coverage.

Personal Injury Protection

Often, it’s called “No-fault” coverage.

It’s mandatory in some states.

Let’s just suppose that you and your friends are involved in a motor accident.

In such cases, if you own this coverage, then it will cover the medical expenses of you and all of the people in the car.

Don’t worry!

It doesn’t matter if you run into another car or another car runs for you.

You can use this coverage in either case.

And that’s not it.

It won’t just cover the medical bills.

Post-accident, it will even cover the rehab, funeral costs, childcare, etc.

And if you are a pedestrian and weren’t in the car, then it will cover you as well.

Medical Payments Coverage

Optional!

That’s what Medical Payments Coverage is.

Let’s learn how this coverage helps you out.

Let’s just suppose that you are involved in an accident.

And you weren’t alone in your car.

Well then! Let me rephrase my sentence.

Let’s just suppose that you and your friends sitting in your vehicle were involved in a car accident.

In such cases, you can use this coverage to cover the medical expenses of just everyone.

It even covers the members who are listed on the policy, also if they were in the other car.

Let me tell you what the best thing about this coverage plan is.

It kicks off after your medical insurance has been all used up.

Let’s just say that your medical insurance has a limit of $100,000 per year.

And the treatment costs $125,000.

Then, this coverage will cover the extra $25,000 that’s required.

No Deductibles! No Copays!

It will even pay for the cost of the copay and the cost of the visit to the clinic.

Uninsured Motorist Coverage

According to laws, we all need insurance to drive.

And the disappointing thing is that not all of us follow the laws.

The chances are that you might be involved in an accident with a person that doesn’t own insurance.

How do you then expect him to cover the costs of your medical bills and repairs?

The person will have to pay for everything from his pocket, right?

And that’s where the “Uninsured Motorist Coverage” comes in.

It’s mandatory in some states, whereas in some countries it’s not.

You’ll have to check whether it’s mandatory in your state or not.

Not only will this coverage cover the cost of your repairs, but also it will pay for the injury and death costs.

And that’s applicable in case of a hit-and-run accident as well.

Flood Insurance

And it’s official.

Federal Emergency Management Agency has named floods to be the most common natural disaster in the United States of America.

Rivers overflowing!

Dams & Levees breaking!

Snow melting rapidly!

It can happen in either case.

And if your home is situated in a flood plain, chances are that you already might own flood insurance.

The Federal Government administers it via the National Flood Insurance Program that’s run by FEMA.

Looking to purchase the flood insurance?

You can directly contact your insurer.

However, it’s provided at a federal level.

$250,000. That’s the home coverage limit.

$100,000. That’s the personal property coverage limit.

“Content’s Coverage.” That’s what personal property is referred to as.

It will cover all the content in your house.

Home Insurance doesn’t cover your car in case of a flood.

Not even you park it inside your home.

Comprehensive Car Coverage! That’s what will cover your car in case of a natural disaster.

And if you live in a flood-prone area, you need to opt for the comprehensive coverage right now.

Mechanical Breakdown Insurance

This one is optional.

It’s totally up to you if you want to buy it or not.

You will be required to pay a little extra over time. Let’s just suppose that something goes wrong with your car shortly. In such a case, you can use this coverage to cover the costs.

The car dealers itself offer it in place of an extended warranty.

We can also call it as “Vehicle Repair Plan” or “Vehicle Service Plan.”

This insurance picks off where the limited warranty of the manufacturer has left off.

Gap Insurance

A common type of insurance is what Gap Insurance is.

However, people often get confused by its name.

You might think that the gap insurance is to cover up for the time when you didn’t have an existing car insurance policy.

That’s a big WRONG!

We also call it as “Loan/Lease Gap Coverage.”

It comes in when you lease or buy a new car.

After you buy a new car and take it out of the showroom, we all know how its value drops like a rock.

However, the same is not the case with your car loan or lease.

And that’s the gap covered by the “Gap Insurance.”

Understanding what we are trying to say?

The value of your car will lessen as soon as you leave the showroom. However, you’ll have to cover the entire loan that you asked for. And that’s where gap insurance comes in.

Long term finance plan, like five years or more, is where a gap coverage comes in.

And this coverage plan will also help you in case your car gets stolen.

Conclusion

And that’s it.

These are the different coverages you needed to know about.

And if you think anyone of them is critical, you shouldn’t even hesitate a second to include it in your car insurance policy.

Questions on how to get Cheap Car Insurance? Call the expert Insurance agents at Star Nsurance + Tax at 813-563-5577